The Shadow Default: How Private Credit Is Hiding Bad Loans in Plain Sight - Part 1

Written by Arbitrage • 2026-04-29 00:00:00

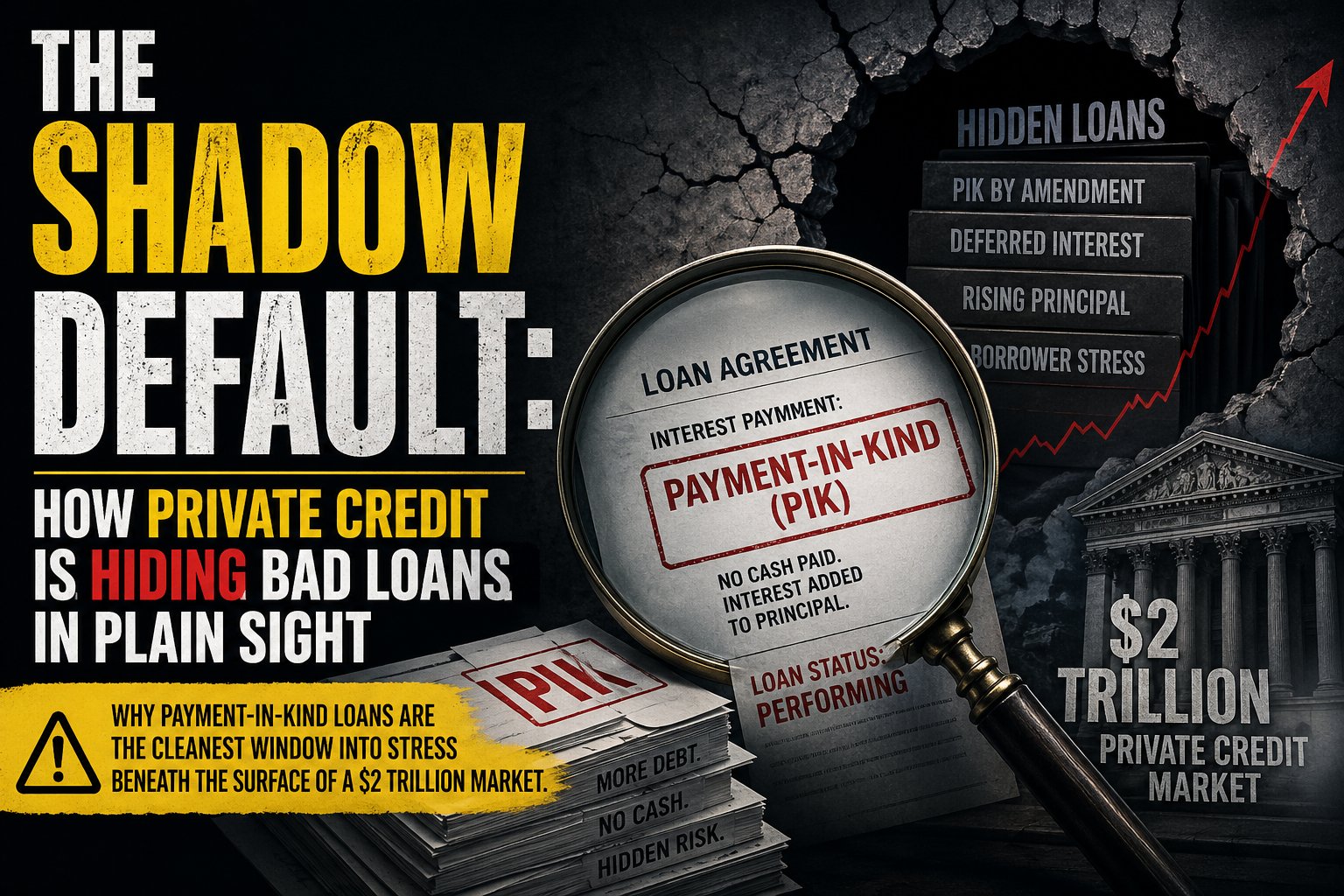

Private credit is supposed to be in good shape. Reported default rates across business development companies sit near historic lows. Headline metrics on the largest direct lending platforms look orderly. The asset class has scaled past $2 trillion, and the official numbers say the loans are performing.

There is one problem with that picture. Roughly 9 to 12 percent of BDC interest income is no longer arriving in cash. It is arriving in the form of more debt added to the principal balance of the loan. The borrower owes more, the lender books income, and the loan stays marked as performing. If borrowers are not sending cash, are these loans really performing? That is the question the rise of Payment-in-Kind interest is forcing investors to ask.

What Payment-in-Kind Actually Is

Payment-in-Kind, or PIK, is a loan feature that lets a borrower defer some or all of their cash interest payment. Instead of writing a cheque, the borrower adds the interest amount to the outstanding principal balance of the loan. The interest still accrues. It just gets capitalized into the debt rather than paid down in cash. Historically, PIK was a feature of junior debt, distressed restructurings, and early-stage growth companies that wanted to preserve cash for capital expenditure. It was a niche tool. The premium PIK loans paid relative to cash-pay loans reflected the additional risk lenders were taking on by waiting for their money.

That is no longer where PIK lives. It is now common in senior secured loans, mainstream direct lending portfolios, and mature borrowers who would have been considered conventional credits a few years ago. There is also a meaningful distinction between two types of PIK that gets buried in headline numbers. PIK structured at origination is a negotiated feature priced into the loan from day one. PIK by amendment is a post-origination conversion of cash interest to PIK, usually at the borrower's request, and the research is increasingly clear that these two patterns carry very different signals.

The Numbers Behind the Surge

The data is the most useful place to anchor this. According to S&P Global, 11.7 percent of loans held by BDCs made PIK payments in the second quarter of 2024, up nearly two percentage points from the same quarter the year before. KBW's analysis estimates that close to 9 percent of private investment income is now being delivered through PIK rather than cash, a level the firm notes is consistent with B-rated bond stress applied across the entire $2 trillion private credit portfolio. iCapital, which sits on the more sanguine side of the debate, suggests investors should treat 10 percent of portfolio loans paying PIK as the threshold for elevated risk. By that yardstick, a meaningful share of BDCs are already past the line.

The trajectory matters as much as the level. Five years ago, PIK was a footnote in BDC quarterly reports. Today it is a standalone disclosure that fund managers spend earnings calls explaining. The composition has changed too. PIK as a percentage of senior secured loans has climbed alongside the headline figure, which means the deferral is no longer concentrated in the riskiest tranches of the capital structure.

Why "Shadow Default" Is the Right Frame

Here is the analytical core. Under current accounting practice, a PIK payment is treated as a valid interest payment. The lender records the income, the loan stays on accrual status, and nothing in the headline disclosures suggests the borrower is under stress. No cash has changed hands, but the books say everything is fine.

This creates what some researchers and risk managers have started calling a shadow default rate. The reported default and non-accrual figures across private credit capture the loans where the borrower has either stopped paying entirely or breached a covenant severe enough to force a restatement. They do not capture the loans where the borrower has quietly negotiated to stop paying cash and start paying with more debt. Both situations involve a borrower that cannot service its obligations from operating cash flow. Only one shows up in the default statistics.

The agency conflict layered on top of this is worth flagging. BDCs mark their own loans, subject to public reporting requirements but with significant interpretive flexibility. They also have a structural incentive to avoid recognizing stress, because the regulated investment company structure requires distributing roughly 90 percent of taxable income as dividends to shareholders. PIK income counts toward that calculation, which means BDCs are paying cash dividends out of interest income they have not yet received in cash. The longer that gap persists, the more dependent the dividend becomes on the eventual repayment of an ever-larger principal balance.

Banks lending to BDCs sit on the other side of this loop. Veteran risk manager Victor Hong has called the practice of accepting PIK as payment "Principal on original Principal," with an obvious shorthand. His point is straightforward. When a bank accepts a PIK payment from a BDC borrower as evidence of loan performance, the bank's balance sheet quietly absorbs credit risk that is not reflected in either entity's reported metrics.

Come back tomorrow for Part 2 of this topic!