The Shadow Default: How Private Credit Is Hiding Bad Loans in Plain Sight - Part 2

Written by Arbitrage • 2026-04-30 00:00:00

If you have not yet read yesterday's blog post, please do so before continuing here.

When PIK Is a Tool, and When It Is a Warning

Not all PIK is bad. The distinction that matters is when the PIK feature was added and why. PIK at origination is a contractual feature negotiated when the loan is first written. The lender prices in the deferral, the borrower gets the cash flow flexibility it needs to fund growth or absorb a cyclical trough, and both sides go in with eyes open. Direct lenders who specialize in growth-stage borrowers have used this structure for years without incident. There is nothing inherently distressed about a PIK loan that was always going to be a PIK loan.

PIK by amendment is a different animal. Research on BDC loan-level data has consistently found that loans where the cash interest obligation is converted to PIK after origination are associated with materially higher rates of subsequent non-accrual status, fair-value markdowns, and bankruptcy. The pattern is strongest where the borrower has no private equity sponsor behind it and where the lender does not also hold an equity stake. In those cases, the PIK conversion is often the first observable sign that the underwriting case has broken down.

Protective factors do exist. Lenders that hold both debt and equity in the same borrower have aligned incentives during a restructuring. Strong covenants, particularly maintenance covenants tied to leverage and interest coverage, give the lender something to negotiate with before a situation deteriorates. Sponsor backing matters. None of these features eliminate the risk, but they meaningfully change how a PIK conversion plays out.

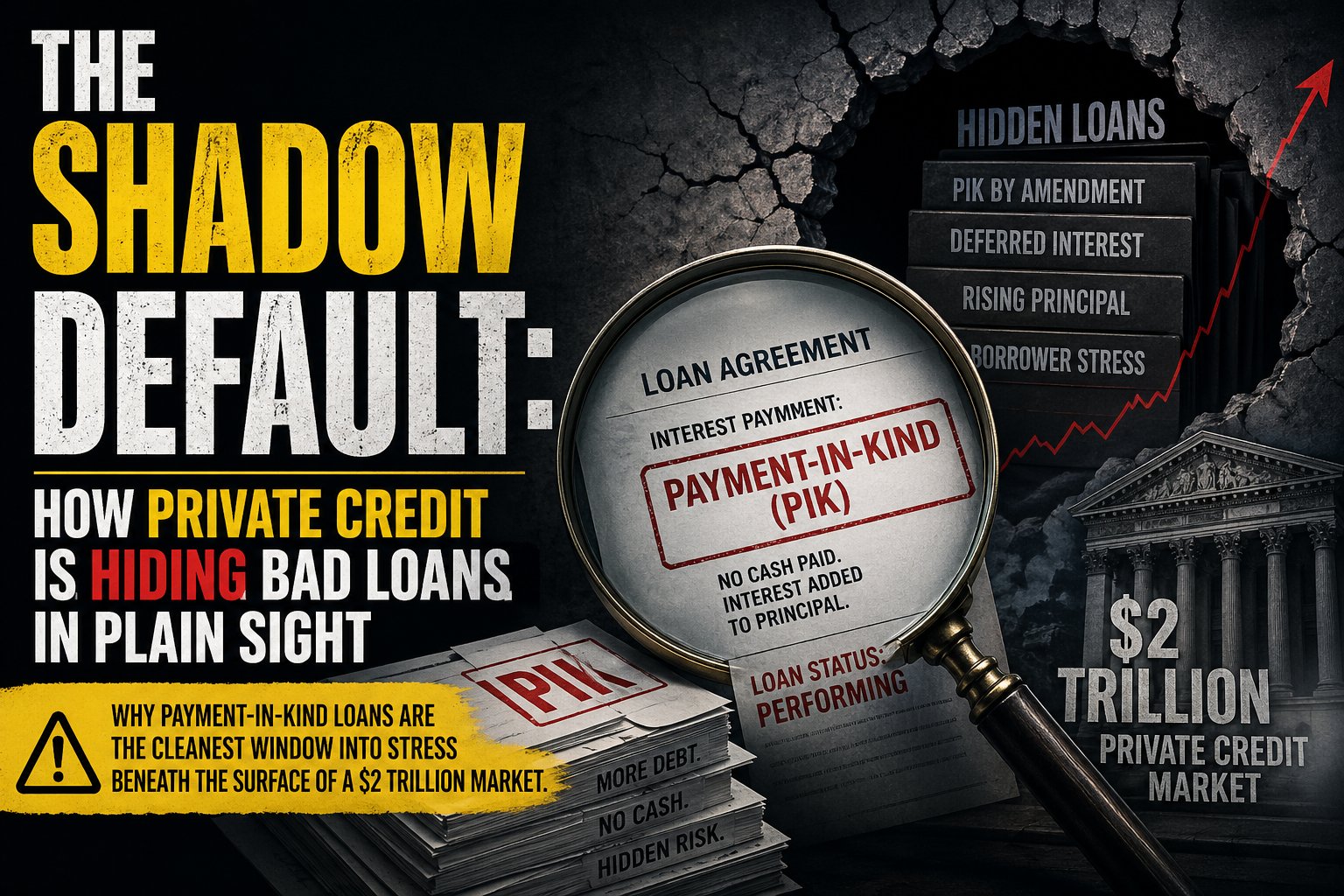

What This Means for the Cycle

Step back from the loan-level mechanics and the macro picture comes into focus. Private credit has scaled into a roughly $2 trillion asset class, much of it floating rate, much of it lent to companies that traditional banks chose not to underwrite. The vintage of loans written in 2021 and 2022 was priced for a different rate environment than the one those borrowers are now servicing. PIK has become the release valve. That release valve has limits. Capitalizing interest into principal works for a borrower that expects to grow into the larger debt load before maturity. It is a different proposition for a borrower whose underlying business is shrinking, whose enterprise value has compressed, and whose maturity wall is approaching. At some point the principal balance grows large enough that even a successful exit cannot repay it in full. The lender has been booking income the entire way through. The eventual recovery, when it comes, sets the price for everything that happened in between.

None of this is fraud. It is the predictable outcome of a financing structure that was designed for flexibility, deployed at scale, into a rate environment that has stressed the borrowers using it. The question for investors is whether the headline default and non-accrual numbers across the asset class are the right place to look for the first signs of trouble. PIK ratios, particularly amendment-driven PIK, are arguably a cleaner window.

The Loans Are Performing

PIK is not a crisis signal on its own. Plenty of loans with PIK features will season normally, get refinanced or repaid at maturity, and never trouble anyone. The point is not that PIK predicts default. The point is that reported default rates and reported income across private credit are quietly understating the underlying conditions, and the gap between the two has been widening for several quarters.

For investors looking at BDC equity, private credit fund interests, or the banks with exposure to non-bank lenders, the PIK ratio is one of the more honest pieces of information in the disclosures. It is also one of the least discussed. Worth tracking.

The loans are performing. The borrowers, increasingly, are not.