The Memory Cycle: How Boom Builds the Bust - Part 2

Written by Arbitrage • 2026-07-08 00:00:00

If you have not yet read yesterday's blog post, please do so before continuing here.

Where the Current Cycle Sits

To read 2026, you have to start in 2022 and 2023. Memory went through a genuine bust. Samsung cut production by something like half. All three major makers pulled hard on investment, and through 2024 and most of 2025 there was little or no new capacity being added. The industry, having been burned, sat on its hands.

Then the AI demand wave arrived, and it hit a market with no slack in it. The mechanism at the center of the squeeze is high-bandwidth memory. HBM stacks DRAM dies vertically, and producing it consumes far more wafer capacity per usable bit than conventional memory. Every wafer pointed at HBM for an AI accelerator is a wafer not pointed at the DRAM in a laptop or the NAND in a phone. By 2026 HBM is running at roughly a quarter of all DRAM wafer production, with demand growing on the order of 70% per year.

The result reads like a textbook upcycle on fast-forward. Contract DRAM prices posted increases in the range of 90 percent quarter over quarter early in 2026, with further sharp gains guided for the second quarter, described by people who track it as the steepest in a decade. Micron printed a record quarter with revenue in the low $40 billions, and HBM sold out for the year. Industry forecasters lifted the memory category by something like 40% for the year.

The live debate is whether this is a structural re-rating or a cyclical peak wearing a structural costume. The bull case is that AI has permanently raised the baseline of memory consumption, that multi-year contracts have replaced spot-market volatility, and that supply discipline among three makers is real. The bear case is that none of those things repeal the cycle, they just stretch it. Both cases describe conditions, not certainties, and a careful read holds them at the same time.

Boom Builds Bust, Applied to Today

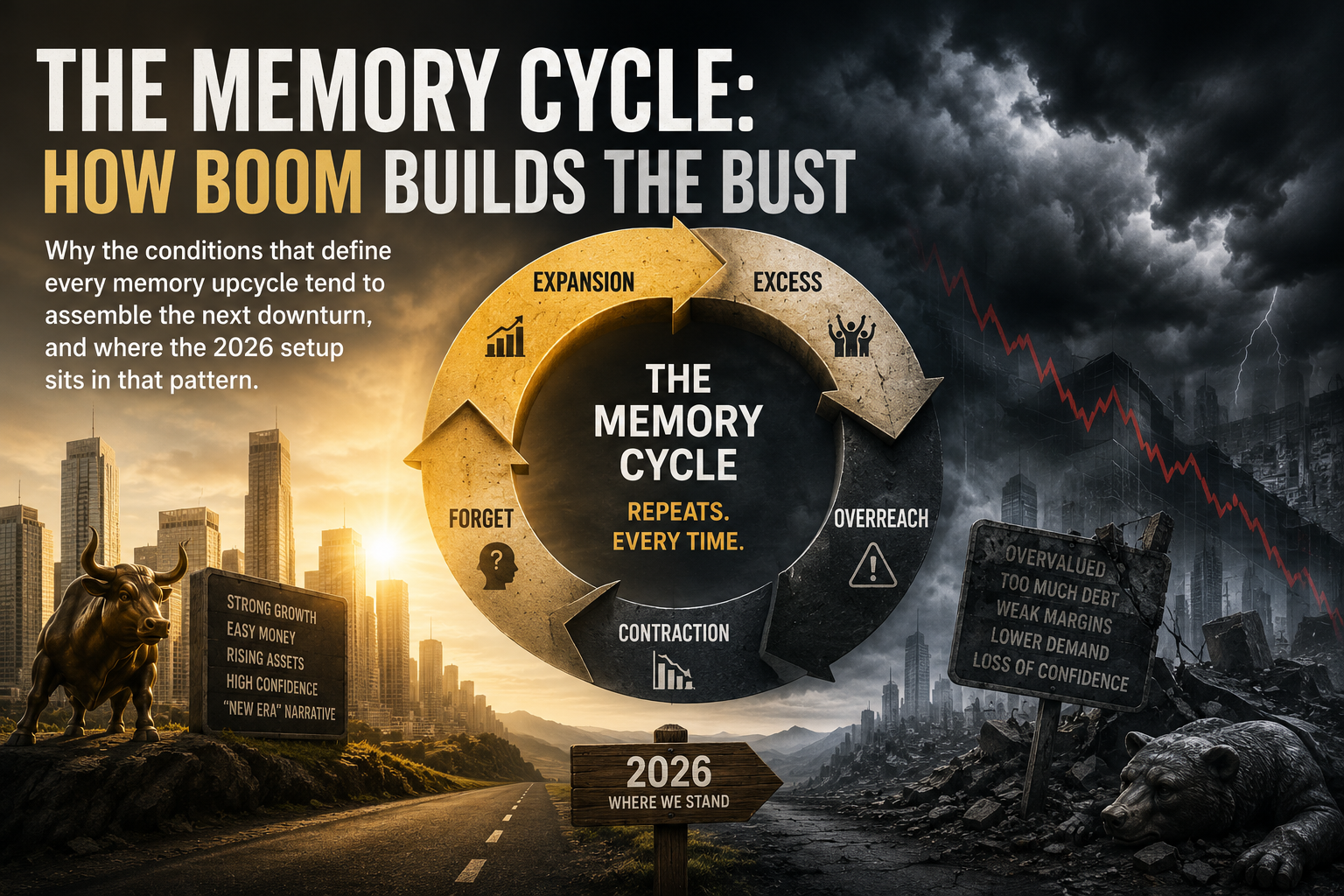

Here's where the title earns its keep. The very things being cited as evidence that memory has escaped its cycle are the classic preconditions for the next downturn.

Record margins are funding record capex. New fab capacity from the major makers is generally expected to arrive in meaningful volume across 2027 and 2028, with some of the largest projects not at full output until the end of the decade. That capacity is being committed right now, at peak pricing, on the assumption that demand keeps compounding.

Two variables decide how the next phase looks. The first is timing: when the new wafers actually land relative to where demand is by then. The second is the demand curve itself, specifically whether AI buildout keeps accelerating or flattens. If supply additions and a demand plateau happen to arrive together, that's the historical recipe for the down leg, and more than one industry veteran has said as much out loud.

One asymmetry is worth holding onto. Memory prices have historically fallen more slowly and more reluctantly than they rise. That shapes what a downturn would actually feel like. Less a cliff, more a long grind, with pricing giving back gains over quarters rather than days. It's a pattern, not a forecast, but it's a pattern with a long track record.

Reading the Names

It helps to separate the names that make memory from the names that consume it.

On the supply side, Micron is the cleanest listed proxy for the memory cycle, a near pure-play that the market tends to treat as the cycle's barometer. SK Hynix sits as the leading HBM supplier with the strongest position in the flagship AI parts, and Samsung is the scale player working to hold its share. These three are the swing producers whose investment decisions, taken together, write the supply side of the next chapter.

NAND runs its own version of the same script. SanDisk, now a standalone storage-memory name, has ridden the enterprise-SSD pull from AI data centers and posted a move that, in percentage terms, has at times outrun even the DRAM names. Same cycle logic, different flavor of memory.

On the demand side sit the accelerator makers. NVIDIA and AMD are where the HBM pull originates. Each new GPU generation tends to ratchet up the memory consumed per chip, which means their product roadmaps effectively set the memory demand curve. When you read that a new B-series or MI-series part needs more HBM stacks than the one before it, that's the demand side of this cycle being written in real time. Whether that pull keeps compounding is the single biggest input into where memory goes from here.

None of this is a view on any individual name. It's a map of where each one sits in the same cycle.

Signals Over Forecasts

If the cycle can't be forecast cleanly, and it can't, the workable approach is to watch the handful of conditions that have historically turned before the story did. The first is the contract versus spot spread, often the first thing to move when pricing pressure builds. The second is capex guidance from the three makers, which tells you how much supply is being committed and roughly when it lands. The third is inventory days, which whisper before they shout. The fourth is the HBM mix within each maker's output, where today's margin actually lives and where it would erode first.

The point of this piece isn't to call a top or a bottom. It's to hold a single idea steady. The conditions that have defined every prior memory cycle - lumpy supply meeting smooth demand, capital committed at the peak, equities re-rating a commodity as a permanent winner - haven't been repealed by this one. They've just been written larger than ever before. Boom and bust aren't opposites in this industry. They're the same process seen at two different points in time.

This too, the man said, will pass. The harder questions are when, and from what altitude.

This piece is illustrative market analysis and pattern recognition, not investment advice or a recommendation to buy or sell any security. Names are referenced to illustrate cyclical dynamics, not as directives. Examples are illustrative only. Conditions described may change without notice. Arbitrage Trade and its contributors may hold positions in securities mentioned.